Throwing Money Away (Buying vs Renting)

I’m tired of hearing people explain that paying rent is throwing money away. Of course, they don’t mean that literally. You’re getting something for that money (a place to live). But with a mortgage you’re building equity, right? Doesn’t that fundamentally make more sense than renting? No. “Building equity” just means turning some of your money into a house. That’s one of many ways you could invest your money.

Practically speaking, there are some reasons why buying instead of renting really is a good idea for a lot of people:

-

Self-binding. Committing to a mortgage may force you to save and invest money that otherwise you would have spent (to spend your house you have to sell it or re-mortgage it). Not that there’s anything wrong with spending money (that’s what it’s ultimately for) but you might well want to force yourself to save more than you’re naturally inclined to.

-

Crazy tax incentives. Mortgage interest is tax deductible in the US and capital gains from selling your home is largely tax-exempt. As part of the current fiscal stimulus plan, many first-time home buyers even qualify for an outright gift from the government of $8000 just to buy a house.

-

Leverage. Buying a house is the only way normal people can invest a huge amount of money on margin. In other words, buying a house means investing hundreds of thousands of dollars of borrowed money in real estate.

-

Control. If you are your own landlord you can’t be forced out or priced out, and you can modify your home as you wish. (The flipside is that it makes your place slightly like the Hotel California — ever leaving will be a serious ordeal.)

But beyond all that, shouldn’t it be cheaper to disintermediate your landlord? In fact, landlord profits are probably a very small part of the equation: on par with the cost of collecting your rent and arranging (not paying for) maintenance. We can check this by seeing how much property management companies charge. Casual web searching indicates it can range from 3% to 15% of rent. But that includes the cost of finding new tenants — the equivalent of which home-buyers pay in spades in realtor commissions (directly or indirectly). I think it’s safe to say that only a few percent or so of your rent is wasted in that sense. Perhaps more or less depending on how often you move.

In a sane market, mortgage interest [net of home apprecation rate; see below] plus property taxes plus maintenance costs will roughly equal rent. None of those expenses build equity any more than rent does.

So paying rent is not fundamentally throwing money away, though it may be leaving free money from the government on the table.

Epilogue

The above was pure armchair excogitation. I’m now the proud renter of an apartment in Harlem at $2500/month, which we also have the option to buy for $600k or so. The condo maintenance fees would then be $1000 or so per month. Property taxes and the mortgage tax deduction roughly cancel out for me. This puts the monthly (unrecoupable) cost of ownership at $3500/month — $1000 more than rent.

For that to make sense, the condo has to appreciate at 2%/year indefinitely. I’m not inclined to make that bet.

To reiterate my original point: buying means $3500/month “thrown away” (in the sense that rent is thrown away). When our agent was telling me these numbers he kept repeating the myth that “if you’re going to spend that money on rent every month you might as well be building equity”. Absolutely false! The fraction of your rent that would go toward building equity (if you put that rent money toward buying instead) is literally less than zero. In places like Manhattan where the rent ratio is high, you’re paying a lot for the privilege of investing in real estate and counting on it to appreciate.

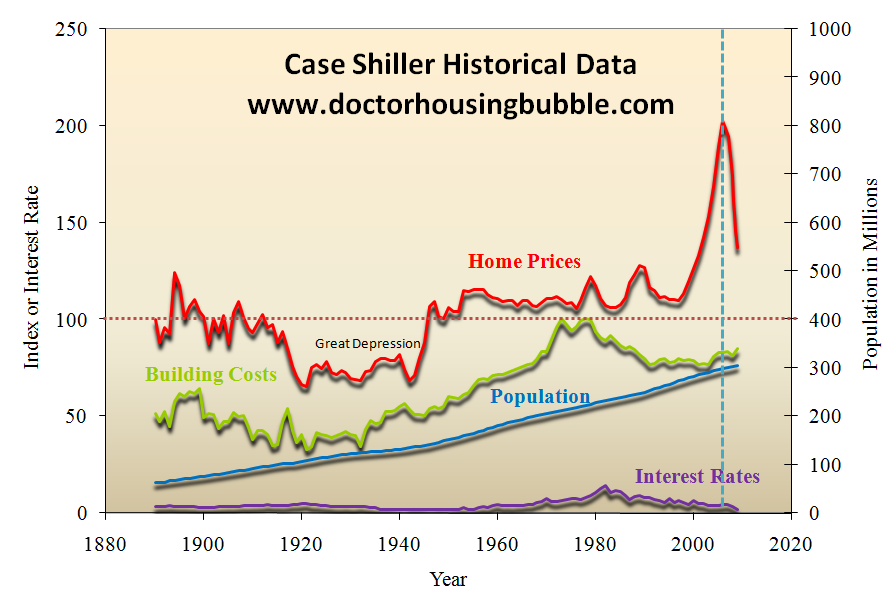

Of course, in a sane market you would count on appreciation in line with the historical rate. For the US (as a whole), that is not much better than inflation. Still, in the rent vs buy calculation, you should subtract from your mortgage interest rate the historical appreciation rate. Unless you believe we’re still in a housing bubble, in which case you should subtract nothing, or even add to the mortgage interest rate.

Two more myths busted for the price of one

Myth: By buying a house your costs go down over time as you pay down the principal on the mortgage.

When people defend the “renting is throwing away money” myth, there are a couple of supporting myths they cite in support of it. First is the related claim that by buying a house your costs go down over time as you pay down the principal on the mortgage. This is wrong. It doesn’t account for opportunity costs. Remember that if you were making alternative investments then you’d be raking in enough money in interest to cover most of your rent by the time your home-buying alternate self paid their mortgage off. More generally, the term of your mortgage (or whether you need one at all) doesn’t much factor in to the buy vs rent decision. You can compare renting vs buying as if you’re getting a zero-amortization mortgage. I.e., assume you’ll be paying only interest and never touching the principal so that your mortgage payments are 5% (or whatever rate banks charge these days) of your home’s value per year forever. Whether you have such a hypothetical infinity-year mortgage or a 30-year mortgage or pay up front with a suitcase full of cash doesn’t matter. A long mortgage term means a lot of interest paid but the suitcase full of cash means a lot of interest you would’ve earned forgone. It’s all a wash.

That does, however, ignore the tax advantages of a mortgage. In fact, a zero-amortization mortgage maximizes the mortgage interest tax deduction, which is probably the biggest factor pushing towards buying.

Myth: Building equity in a house beats alternative investments.

The second related myth, and another common rationalization for buying over renting, is the claim that real estate is a fundamentally better investment (and so building equity in a house beats alternative investments). This claim doesn’t hold up, even if you made the (unwarranted) assumption that house prices have bottomed out. You always have the ability to invest in real estate without buying a house.

Illustration by Kelly Savage.

Thanks to David Reiley, Alex Strehl, Andrew Reeves, John Langford, Bethany Soule, Martin Reeves, Dave Pennock, Laurie K. Reeves, Sharad Goel, Bob Soule, Rob Felty, Kevin Lochner, and Jake Hofman for helpful discussions and home-buying anecdotes.

UPDATE: There are excellent points and additional resources and caveats in the comments. Thanks! I added one myself clarifying why “buying gets cheaper eventually as you pay off the mortgage” is wrong. I stand by the original point: If you ignore price bubbles, taxes, personal preferences, and leverage then renting and buying are roughly financially equivalent. Not that you should ignore those things, just don’t fall for the myths that it’s a no-brainer decision.

UPDATE: Now in Spanish, thanks to ManzanaMecanica.org [RIP].

{kind=link}

{kind=link}